Business leaders across the world are riding a wave of optimism about the power of new technologies to drive growth and competitiveness. The 2025 VivaTech Confidence Barometer, a survey of 1,700+ executives in Europe and North America, reveals a remarkably high level of trust in tech, with an overall confidence score of 87 out of 100. In the past year, 81% of these executives say their appreciation for the role of emerging technologies in competitiveness has risen. They see digital innovation not as a distant bet, but as a present-day engine of international relevance. This upbeat outlook comes with an insight-led understanding: technology adoption offers tangible benefits like productivity gains and cost savings, but realizing its full potential requires navigating regional disparities, talent gaps, regulatory hurdles, and societal risks.

New Technologies Inspire Optimism and Growth

One of the clearest messages from the VivaTech Barometer is that businesses view technology as a cornerstone of growth and international competitiveness. 81% of surveyed executives believe tech is a key driver of their company’s global competitiveness. This sentiment is consistent across geographies and has strengthened over the past year. In fact, 81% of respondents report that in the last 12 months their perception of new technologies’ importance for competitiveness has improved (a jump of 9 percentage points from the previous year). There is near-unanimous agreement that adopting new tech pays off: 100% of executives surveyed say implementing at least one new technology has yielded tangible benefits, such as higher productivity (cited by 62%) or lower operating costs (48%).

This optimism is not just theoretical, it’s translating into action. 91% of companies plan to boost investment in at least one of the technologies they’re currently using. In other words, virtually every business leader surveyed is doubling down on tech adoption as a growth strategy. The mindset is clear: innovate or fall behind. Even amid economic uncertainties, investment in digital tools is seen as non-optional for staying competitive.

To visually ground this optimism in data, the following chart highlights how executives are currently experiencing and projecting the benefits of digital technologies across key business outcomes:

Notably, technology is viewed as a lever for international expansion and relevance. In a globalized economy, being on the cutting edge of tech can level the playing field for companies from any region. A large majority (81%) of executives believe that leveraging new technologies will enhance their international competitiveness. This belief aligns with external analyses of how digital adoption correlates with export performance and market leadership. For instance, a McKinsey Global Institute study finds that European firms that aggressively scale technology and R&D across borders tend to outcompete others, whereas those constrained by fragmented markets risk falling behind. In short, technology is seen as the gateway to global markets.

Crucially, the optimism extends to seeing tech as a solution to broader societal challenges. More than 90% of executives in the barometer believe technology can be harnessed to address the major challenges of our time. They cite areas like improving education, combating misinformation, and promoting inclusion as domains where tech can empower positive change. This perspective aligns with global initiatives focusing on “tech for good.” The World Bank, for example, highlights AI’s potential to accelerate progress on the UN Sustainable Development Goals, from improving healthcare to optimizing agriculture. There is a prevailing sense that if managed correctly, innovation isn’t just good for business, it’s good for society.

AI as the Flagship of Innovation

Amid the general enthusiasm for tech, one field stands out in 2025: artificial intelligence (AI). The survey data and external indicators all point to AI as the flagship technology of this era, the one most likely to disrupt business and confer competitive advantage. 85% of companies surveyed by VivaTech plan to increase their investment in AI over the next 12 months, making it the top area of tech spending. Executives clearly see AI as transformative: when asked which technology will have the biggest impact on their business in the coming years, 65% chose AI, far ahead of the next contenders like cybersecurity (41%) or cloud computing (39%). The following chart illustrates how AI clearly leads the technology agenda among business leaders in 2025, with cybersecurity, cloud computing, and data analytics following closely behind:

This finding resonates strongly with global trends. AI has vaulted to the forefront of boardroom discussions and R&D budgets. Private investment in AI is at record levels. The Stanford AI Index reports that US private AI investment reached 09 billion in 2024, nearly 12 times the amount invested in China ($9.3B) and 24 times that of the UK (.5B). Worldwide, generative AI in particular saw a surge of venture funding in 2024, attracting nearly 4 billion (an 18.7% increase year-on-year). Businesses are not just talking about AI; they are pouring resources into it, betting that it will boost productivity, automate processes, personalize customer experiences, and open new revenue streams.

For businesses worldwide, what matters is how these dynamics translate into opportunities or threats. The Barometer data suggests most companies feel they cannot afford to sit on the sidelines of the AI revolution. The consensus is that adopting AI now is key to future success, a belief shared across industries from finance to manufacturing. Indeed, 100% of surveyed executives agreed that adopting new tech yields benefits. And looking forward, 85% plan to ramp up AI investment in the short term, indicating that even latecomers are jumping on board. Yet, the rush toward AI and other emerging tech also brings into focus a critical element: the human and organizational factors that determine success. Technology doesn’t operate in a vacuum. Talent, skills, and culture are crucial.

The Human Factor: Talent, Skills, and R&D

Even in an age of automation and AI, human capital remains the linchpin of technological competitiveness. The VivaTech survey makes this abundantly clear: when asked what factors most ensure their company’s tech competitiveness, executives put “highly qualified talent” at the top (45% cited this), followed closely by continued investment in R&D (44%) and a strong international reputation (43%). In other words, it’s not just about having the latest gadgets or software, it’s about having the people who can develop, implement, and leverage those technologies effectively, supported by a culture of innovation and trust. These responses highlight a fundamental truth: technology is only as good as the team behind it. A company might have access to AI algorithms or big data infrastructure, but without skilled employees and visionary leadership, those tools won’t translate into a competitive advantage. Business leaders recognize this; hence the emphasis on talent and research spending as core to tech success.

However, many firms worry that they might not have the talent they need. A lack of qualified employees is cited as a frequent obstacle by 41% of executives surveyed, and internal resistance to change is noted by 39%. This “human factor” challenge is nearly universal: from Silicon Valley to European tech hubs, there is intense competition for AI engineers, data scientists, cybersecurity experts, and other digital skills. The World Economic Forum’s Future of Jobs Report 2025 confirms that skill gaps are viewed as the single biggest barrier to business transformation, with 63% of employers seeing inadequate skills as a major hurdle.

These findings are mirrored by global research, reinforcing the view that talent shortages and transformation fatigue are growing barriers to innovation. The following chart highlights the most pressing human capital challenges reported by executives and forecast across the industry:

In fact, skill gaps outrank other barriers like financial constraints or technology availability in that global survey. Another study predicts that by 2026, over 90% of organizations worldwide will experience an IT skills crisis, potentially resulting in + trillion in lost economic opportunity. These statistics underscore why executives are so concerned about attracting and retaining qualified talent.

To remain competitive, companies are ramping up efforts in reskilling and upskilling their workforce. Many large firms have launched internal academies or partnerships with online learning platforms to train their staff in AI, cloud, and data analytics. The Barometer data hints at this: 9 in 10 companies report they have already put in place measures to inform and reassure employees about new technologies, which often involves training programs to help employees adapt and overcome resistance. Business leaders understand that people power technology. The confidence in tech’s promise comes with a clear-eyed view that investing in human capital through hiring, training, and R&D is non-negotiable for success.

A Two-Speed Tech Landscape: United States vs. Europe

While confidence in technology is broadly high, the VivaTech Barometer reveals striking regional disparities. Executives in the United States express the highest confidence in their nation’s tech competitiveness, whereas within Europe, optimism varies markedly from one country to another. The result is a two-speed tech landscape: the US (and to an extent Canada) charging ahead, parts of Europe keeping pace, and others lagging behind. Understanding these differences is crucial for a global view of tech trends in 2025.

According to the 2025 VivaTech Barometer survey:

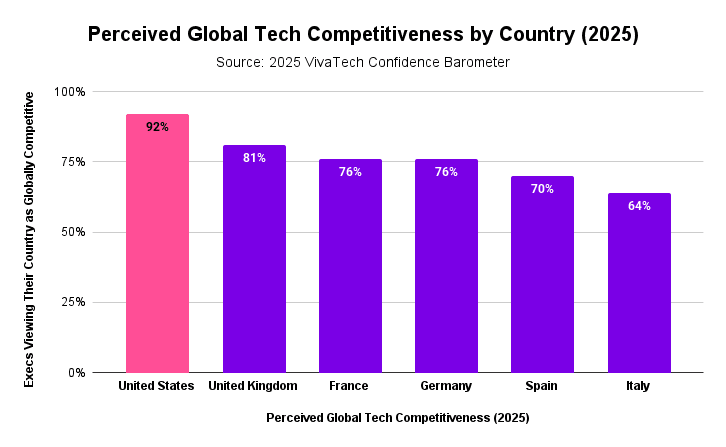

92% of American tech executives believe their country is at the forefront of international tech competitiveness. This is an extraordinarily high self-assessment, and notably up from 86% the previous year, indicating growing confidence. It suggests that US business leaders see America leading the world in tech.

The United Kingdom ranks next, with 81% of British CEOs considering the UK at the forefront of tech. The UK, home to fintech hubs and AI research labs like DeepMind, apparently punches above its weight in confidence, even slightly ahead of larger EU economies.

France and Germany come in around 76%, with roughly three-quarters of their executives feeling globally competitive. Spain is slightly lower at 70%.

Italy, however, markedly trails with only 64% of Italian CEOs judging their companies competitive internationally. Moreover, just 44% of Italian execs see Italy as a leader in adopting technological innovations, by far the lowest of all countries surveyed. Italy clearly perceives itself as falling behind the pack.

The following chart compares executive perceptions of global tech competitiveness across six major economies. While confidence remains high overall, the regional spread highlights clear disparities in strategic positioning and digital maturity.

So, why is the United States brimming with confidence compared to, say, Italy? Several factors likely play a role:

Scale and investment: US companies dramatically outspend European ones in R&D and tech deployment. American tech giants dominate global markets and set industry standards. This translates into a feeling of leadership. European firms, on average, are smaller and invest less in new tech, which can breed caution. A WEF/McKinsey analysis found that large European firms invest $400 billion less per year than US firms, and spend only half as much of their revenue on R&D. European CEOs themselves recognize this shortfall. In one survey, 84% of European CEOs said the continent’s competitiveness is weakening, citing a “complex and/or incoherent regulatory environment” as a key reason.

Unified market vs. fragmentation: The US enjoys a large, unified domestic market where a successful tech product can scale nationally before going global. Europe, despite the EU single market, still contends with linguistic, cultural, and regulatory fragmentation that can slow scaling. For example, a startup in Europe often must navigate 27 different regulatory regimes, whereas a US startup deals with one federal system (plus state nuances). This fragmentation is one reason Europe has fewer big tech companies and perhaps why countries like Italy, with less developed tech ecosystems, feel left behind.

Regulation and risk appetite: The US traditionally takes a more laissez-faire approach to tech, encouraging experimentation and “move fast, break things” innovation. Europe has been more inclined to regulate early and heavily (data privacy, antitrust, AI ethics, etc.), reflecting a different societal preference for caution. This has advantages in protecting consumers, but some argue it can stifle innovation and make businesses more hesitant. Indeed, as the Barometer points out, US executives increasingly cite regulatory compliance and data protection requirements as major obstacles (50% say these are the main hurdles to adopting emerging tech, up 12 points from last year). In other words, even Americans are feeling some regulatory friction (perhaps as global data laws like GDPR affect them), but European firms have navigated such constraints for longer.

Innovation hubs and talent magnets: The US hosts many of the world’s top innovation clusters like Silicon Valley, Seattle, Boston, and New York, that continuously spin out new companies and attract global talent. Europe has excellent hubs (Berlin, Paris, Stockholm, London, etc.), but talent flow is often outbound (Europe has historically seen brain-drain of tech talent to the US). Countries that manage to retain and attract innovators, like the UK and France in recent years, can build more confidence. Italy’s tech sector has been comparatively less vibrant, which may affect executives’ outlook.

It’s worth noting that the VivaTech barometer did not survey Asia or other regions, so the “two-speed” discussion here is focused on the West. If Asia were included, China would likely register high confidence as well, given its huge strides in 5G, AI, and digital platforms (though tempered by recent regulatory crackdowns in tech). Many emerging economies are also rapidly digitizing, but they may express optimism of a different kind. For example, African tech leaders might be confident in leapfrogging with fintech and mobile innovation, even if they lack the infrastructure of richer nations. For the scope of this report, however, the US-Europe comparison is central.

Striking a Balance on Data Governance and Regulation

As businesses race to adopt AI and other technologies, they increasingly confront the thorny issues of data governance, privacy, and regulation. The VivaTech survey highlights a paradox that many tech leaders recognize: technological progress is essential and strategic, but it also raises new risks and regulatory challenges that cannot be ignored. Navigating these successfully is critical to maintaining confidence and momentum in the tech sector.

Data is the lifeblood of the digital economy, and how it’s governed has become a strategic question. In the survey, executives across countries expressed equal levels of concern (77%) about two things: the invasion of privacy and the proliferation of fake news. Privacy concerns stem from the massive amounts of personal data being collected and analyzed by AI systems, IoT devices, and platforms. Businesses know that if they misuse data or suffer breaches, they will lose consumer trust and face legal consequences. Indeed, over half of companies expect data management to grow even more complex in the near future, a nod to evolving data protection laws and rising public scrutiny.

Different regions have taken different approaches to data governance:

Europe has led the world in data regulation with the General Data Protection Regulation (GDPR). Since 2018, GDPR has set a high bar for data privacy, enforcing principles like consent, data minimization, and the right to be forgotten. It applies not just to European companies but to any company handling EU residents’ data, effectively globalizing its impact. The EU is building on this with more frameworks like the Digital Markets Act, Digital Services Act, Data Governance Act, and the forthcoming AI Act; all aiming to create a trusted digital environment. The upside is greater user trust and ethical standards; the challenge is the compliance burden on companies.

The United States historically took a lighter touch to tech regulation, favoring innovation and self-regulation over heavy-handed rules. There is no US equivalent of GDPR at the federal level (though states like California have enacted strong privacy laws). However, attitudes in the US are shifting somewhat. With rising concerns over AI ethics, misinformation, and antitrust issues with Big Tech, American lawmakers and regulators are engaging more. We’ve seen congressional hearings on social media’s harms, new FTC scrutiny of tech mergers, and discussions of AI oversight bodies. Still, relative to Europe, the US regime is considered more pro-innovation and less restrictive. Some analysts argue this has been key to US tech leadership, cautioning that over-regulating too early (as they claim the EU does) might hinder competitiveness.

The clash and contrast of these philosophies is evident in international debates. As the WEF observed, different approaches to digital governance have “deepened geopolitical competition between the US, China, and the EU.” However, there are ongoing efforts to find common ground:

The EU-US Trade and Technology Council (TTC) is one forum where transatlantic allies are trying to bridge differences in tech governance. For instance, after legal tussles invalidated the prior EU-US data sharing agreements (Safe Harbor, Privacy Shield), the two sides recently agreed on a new Data Privacy Framework to facilitate data flows with stronger safeguards. This is crucial for businesses that operate internationally, as they need clarity on how to legally transfer data (think of a European subsidiary of a US company sharing data with HQ; rules must be clear to avoid fines). The new framework aims to appease European privacy concerns by limiting US government access to EU citizens’ data.

On AI governance, there are calls for international coordination. The OECD has published AI principles adopted by dozens of countries, emphasizing concepts like transparency, safety, and accountability in AI systems. In 2025, the OECD even launched a voluntary AI risk reporting framework for companies, encouraging them to disclose how they mitigate AI risks. Such moves recognize that AI development is global and no single country’s rules will be sufficient if others don’t follow suit.

For businesses navigating these waters, a few strategies have emerged:

“Privacy by design” and robust compliance: Companies are building privacy and security features into their products from the ground up, not just as an afterthought. This not only avoids legal trouble, but can be a competitive advantage as consumers increasingly value privacy.

Engagement in policy discourse: Tech executives are no longer staying aloof from regulation; they are actively engaging with governments. We see CEOs testifying in hearings, industry groups contributing to AI ethics guidelines, and cross-industry coalitions forming to help shape reasonable regulations. This is a strategic response to ensure that rules set by governments are informed by technological realities and do not inadvertently stifle beneficial innovations.

Global data strategies: Companies are revisiting how they handle data internationally. Some are localizing data storage to comply with sovereignty laws (e.g., keeping EU data in EU data centers). Others are investing in emerging solutions like federated learning (where AI models train on local data without it leaving the source) to reduce the need for raw data transfer.

Confidence in tech’s future is intertwined with confidence in managing its risks responsibly. The Barometer’s findings that executives are highly concerned about privacy and misinformation, but are also proactive (90% have measures in place to educate and reassure stakeholders), show that the industry is not blind to these issues. There is a collective understanding that trust is the currency of the digital economy: users and customers will embrace new tech only if they feel their data is safe and their society isn’t being harmed by it.

This dual focus on opportunity and accountability is central to the privacy paradox. While executives are doubling down on innovation—particularly in AI—they are equally focused on mitigating risk and restoring public trust. The chart below visualises this strategic tension:

Battling Misinformation and Building Trust

The digital revolution has greatly democratized information, but it has also unleashed a plague of misinformation and disinformation that poses risks to businesses and society alike. The VivaTech Confidence Barometer highlights this as a top concern: three-quarters of surveyed executives (77%) are worried about the spread of fake news and the difficulty in identifying what’s true.

Misinformation can directly impact companies. Consider how false rumors can sway stock prices or how misinformation about technology (say, vaccine microchips or 5G conspiracies) can hinder the rollout of innovations. On a broader scale, business leaders, as part of society, are alarmed by how disinformation can undermine democracy and social stability.

The Barometer data shows some interesting nuances:

Concern about fake news is especially high in the United States (83% of American execs express concern, up 5 points from last year) and in Spain (90%). These could be reflections of recent experiences, the US has grappled with election-related disinformation and COVID-19 conspiracies, and Spain l has also dealt with its share of misinformation in a polarized environment.

Germany and Italy are comparatively less concerned (59% and 67% respectively). It’s not that misinformation isn’t present there, but German business culture may have more confidence in media literacy or benefit from strong public broadcasters; Italy’s slightly lower concern could be due to other pressing issues taking precedence, or perhaps an underestimation of the threat. France remains concerned (79%), though interestingly, that number fell a bit from 83%, possibly reflecting efforts to address the issue.

The UK and Spain show the highest conviction (52% in each) that tech can help combat misinformation by improving access to accurate information. This suggests hope that tools like AI can be double-edged: yes, they can create deepfakes, but they can also detect fake content and amplify factual content.

In response to the misinformation challenge, companies are not sitting idle. The survey notes that 9 out of 10 companies have implemented measures to inform and reassure their employees, clients, or service providers regarding technology and information authenticity. These measures vary but often include:

Media literacy and training programs: Some firms conduct workshops for employees on how to identify phishing attempts, deepfakes, or misleading information online. This not only protects the company (cybersecurity) but also empowers employees as citizens to navigate digital information critically. The OECD recommends exactly this approach, strengthening media and information literacy to inoculate the public against false information.

Internal communications and fact-checking: Companies have ramped up internal fact-checking for communications and created channels where employees can ask questions about rumors. For instance, during the pandemic, many organizations sent regular bulletins dispelling myths (using credible sources) to keep their workforce correctly informed.

Collaboration with tech platforms: Businesses, especially advertisers, pressure social media platforms to police misinformation, as brand reputations can suffer if ads run next to extremist or false content.

Ultimately, combating misinformation ties back to the core theme of trust. In the context of the Confidence Barometer, despite worries, it is noteworthy that 90% of business leaders still view technology as a solution to major societal challenges, including fighting misinformation itself. This reflects a nuanced view: technology created these new problems, but technology guided by enlightened leadership and ethical norms can also fix them. Supporting this optimism, examples abound of tech-driven initiatives that improve information integrity:

Crowdsourced fact-checking communities and better tools for journalists.

Transparency measures (like Meta’s ad libraries or Google’s Ad Transparency Center) make it harder for falsehoods to go unchecked.

Winning the fight against misinformation is seen as integral to maintaining a healthy digital ecosystem where technology can flourish. If people trust what they see and read online, they will be more open to new digital services and products. Therefore, tackling fake news is not just a social imperative but also an economic one for the tech industry.

Technology as a Solution to Global Challenges

A striking finding in the VivaTech Barometer is the overwhelming agreement that technology is not only an engine of business but also a potential solver of societal problems. Over 90% of surveyed executives believe tech can provide solutions to the big challenges of our era. This perspective is crucial because it frames the mission of innovation in a broader, more purpose-driven context. If tech confidence can be channeled into tackling issues like climate change, education gaps, and inequality, it bodes well for aligning the tech industry’s goals with the needs of society.

We’ve already seen how leaders think tech can combat misinformation and improve education (42% and 45% of respondents respectively noted those as areas tech can empower people). Let’s consider a couple of other global challenges where tech optimism is high and growing. These findings reflect a growing belief that digital innovation should serve not only business outcomes but also societal good. The following chart shows which global challenges executives believe technology is best positioned to help solve:

1. Climate and Environmental Sustainability: Technology is both a contributor to climate issues (think of data centers’ energy use) and a vital part of the solution (renewable energy tech, smart grids, climate modeling, etc.). The Barometer reveals that 70% of business leaders are concerned about tech’s negative environmental impact. This concern is especially pronounced among startups and unicorn companies, nearly half of those expressed being very concerned.

Companies are increasingly committing to carbon neutrality and using data analytics to cut emissions in their operations. The fact that the US showed a big jump in environmental concern (74% in 2025, up from 57% in 2024) indicates a rising consciousness that spans the Atlantic. Global collaborations, such as tech firms joining the Climate Pledge or the development of international green computing standards, are part of a strategic response to ensure technology helps heal the planet rather than hurt it.

2. Health and Education: The COVID-19 pandemic accelerated digital transformation in health (telemedicine, mRNA vaccines, data-driven public health) and in education (online learning platforms, education content apps). This opened many eyes to how tech can address systemic challenges. Now, healthtech and edtech continue to be vibrant areas. Business leaders in Germany, for instance, are particularly convinced of tech’s role in improving education, 60% highlighted education as a domain for tech solutions, above the average.

We also see cross-sector initiatives: big tech companies partnering with governments to bring broadband to rural areas (bridging the digital divide is key to both education and economic opportunity). There’s also optimism around AI in drug discovery and personalized medicine, which could revolutionize healthcare globally. The “Tech for Good” movement, championed at forums like VivaTech and WEF, encourages startups to focus on social impact areas, often with support from corporate and government innovation funds.

3. Inclusion and Equality: One might not instinctively see technology as the cure for inequality. Indeed, it can sometimes widen gaps, but the survey shows a notable trend. In France, there’s a growing emphasis on using tech to promote diversity and inclusion, with 32% of French execs citing this in 2025, up from 18% the year before. Additionally, 81% of CEOs across countries believe the tech ecosystem overall promotes diversity and inclusion.

How so? Perhaps through democratizing information, enabling remote work, and providing platforms for underrepresented voices. For example, AI can help detect and reduce biases in hiring or lending, if used conscientiously. Social media and e-commerce lower barriers to entry for entrepreneurs from diverse backgrounds to reach global audiences. Of course, this optimism comes with the caveat that conscious effort is required to ensure inclusivity (hiring practices in tech, making sure AI datasets are unbiased, etc.). Yet the belief that tech can be a great equalizer is heartening. It aligns with initiatives like expanding internet access (there are still billions without reliable internet) which is foundational to inclusion. The World Bank and others emphasize digital inclusion as a path to poverty reduction and empowerment.

Strategic Tech Responses Globally:

To harness technology for these challenges, both public and private sectors are mounting strategic responses:

Governments are crafting national AI and digital strategies that explicitly link innovation to the public good. For instance, the EU’s digital strategy speaks of developing “trustworthy AI” to enhance competitiveness while safeguarding democratic values. Many countries (from Canada to Singapore to Kenya) have set up AI ethics committees or task forces to guide responsible tech deployment.

There is a push for public-private partnerships. Large tech firms are working with international organizations to, say, apply AI for climate resilience or use big data to predict and prevent disease outbreaks. These partnerships are crucial because solving societal issues often requires resources and expertise beyond what governments alone possess.

Companies themselves, especially those brimming with tech confidence, are broadening their corporate missions. The idea of stakeholder capitalism, where businesses aim to serve not just shareholders but all stakeholders (customers, employees, communities, and the environment) dovetails with using tech for positive impact. We see tech CEOs pledging to fund AI research for social good, or open-sourcing certain technologies to help spread beneficial tools (for example, when companies open-source AI models for healthcare research).

Global forums like VivaTech are increasingly centering discussions on how to maximize the upside of technology while mitigating downsides. This synergy between confidence and caution is precisely what will determine if tech truly delivers on its promise.

The strongest insight here is that the tech community’s confidence is matched by a sense of responsibility. Far from being caught in narrow tech-boosterism, today’s business leaders appear to grasp that long-term confidence in technology will only be maintained if technology visibly improves lives and addresses urgent crises, all while respecting fundamental values like privacy, security, and equity.

Conclusion: Moving Forward with Confidence and Caution

The breadth of findings and perspectives we’ve explored paints a picture of buoyant optimism in the power of technology, coupled with clear-eyed awareness of challenges. In 2025, tech and business leaders are largely confident that innovation will drive growth, that AI will unlock new frontiers, and that their companies can compete on the world stage. This confidence is quantifiable (87/100 confidence index, rising investment stats) and palpable in boardrooms across the globe.

Yet, this is not blind optimism. It comes with a healthy dose of realism about what it takes to succeed and what could impede progress:

Leaders know they must invest not just in shiny new tech, but in people and the skills and creativity of their workforce.

They recognize the uneven landscape and are pushing to bring everyone along, whether that means uplifting lagging regions or ensuring smaller enterprises aren’t left behind in digital adoption.

They are grappling with how to govern technology’s impact, striving to find the sweet spot where innovation and regulation reinforce each other, rather than clash.

And importantly, they see technology as integral to solving problems, not just making profits. This broader vision is critical for keeping society’s trust.

For Europe and the United States, the narrative that emerged is one of different speeds but potentially complementary strengths. The US leads in raw innovation and scale, Europe leads in thoughtful regulation and collaborative approaches; both need to learn from each other. A transatlantic (and indeed global) dialogue on AI governance, data flows, and digital standards will be vital to ensure we don’t fragment the digital world or stifle progress with divergent rules.

What are the strongest insights to carry forward from this analysis?

Tech Confidence is High and Rising: Business leaders overwhelmingly believe in tech as a growth catalyst. Even turbulent times haven’t dampened that faith if anything, the pandemic and economic swings reinforced the value of agility through technology.

AI is King, but Not the Only Game: AI dominates investment and mindshare, yet it accentuates the need for talent, for infrastructure (data centers, energy), and for prudent governance. Those who master AI’s use are likely to set the pace in many industries.

Human Capital and Culture Make the Difference: Access to technology is widespread, but the ability to exploit it distinguishes the winners. Countries and companies that cultivate talent, embrace change, and foster innovation networks will lead, as evidenced by the US’s edge and Europe’s internal variations.

Mind the Gap, and Close It: Regional and sectoral disparities in tech adoption are pronounced. There is nothing inevitable about these gaps. They are the result of policy choices, education, investment, and risk appetite. With targeted effort (like investment in lagging regions, regulatory reform, or incentive structures), gaps can be narrowed. The surge in confidence in some European countries shows that positive momentum is possible.

Trust and Tech Go Hand in Hand: The long-term sustainability of the tech boom rests on maintaining public and stakeholder trust. This means doubling down on data protection, cybersecurity (interestingly, cybersecurity was seen as the #2 tech as likely to impact business at 41%, itself a recognition that without security, innovation falters), and fighting disinformation. The fact that misinformation is viewed as a top global risk is a clarion call: we must secure the info sphere for any digital strategy to succeed.

Tech for Good is More Than a Slogan: It’s becoming a strategic pillar. CEOs are not merely acquiescing to social responsibility; they are actively strategizing around it, whether to meet ESG goals, attract talent (young professionals often want to work at mission-driven companies), or open new markets by solving tough problems.

In crafting a way forward, leaders in tech and policy might consider a few guiding thoughts:

Collaborate on Standards and Innovation: Competition should not preclude cooperation on foundational issues. For example, agreeing on AI safety standards or data sharing protocols can benefit all, much like nations cooperated on standards for aviation or telecom in earlier eras.

Invest in Resilience: The high confidence in tech is justified, but recent years have taught us about resilience. Cyber attacks, supply chain chokepoints (semiconductors), and even pandemics can derail tech progress. Building resilient systems that are secure, diversified, and sustainable will protect the confidence we have in technology’s benefits.

Inclusivity as Strategy: Ensuring more stakeholders (countries, smaller firms, marginalized groups) are included in the tech revolution isn’t just altruism; it grows the pie of innovation. The more brains working on problems, the better. Plus, avoiding a digital divide reduces the risk of backlash against technology.

Lifelong Learning Revolution: To keep up with technology, education and workforce development need continuous innovation. The most confident companies are often those that have become learning organizations. We see an imperative for society-wide upskilling initiatives so that the workforce of 2030 is ready for the jobs of 2030, many of which will revolve around technologies just emerging now.

The 2025 VivaTech Confidence Barometer offers a hopeful message: in the eyes of those steering the world’s companies, technology remains a trusted ally and a beacon for the future. The insights and evidence we’ve compiled show a community well aware of its duties and challenges. If stakeholders can maintain this balance of enthusiasm and responsibility, then the confidence we see today will be vindicated by achievements tomorrow.

The task now is to ensure that technology’s reach is matched by our collective grasp of wisdom. With that, the world can indeed move forward with both confidence and caution, harnessing the full power of tech for global good.